“Let's say an energy supplier runs an atomic power plant, and that it cost 1000 money-units (MU) to build. The energy supplier assumes that he'll be running the plant for 25 years. Half of the plant was financed via a bank loan. The personnel costs of running the plant are 30 MU per year, and at the start of the project there's 50 MU cash available. These details yield the following start-up balance:

Net assets (or equity) consist here of half the power plant plus the cash position. Now let's assume the interest rate of the loan is 5% per year, and that the term is 25 years. The energy supplier earns from his tariffs a yearly revenue of 120 MU. His profit and loss account would look, at the end of the first year, like this:

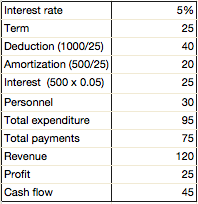

The startup costs of the long term capital are spread out, via amortization, over the plant's economic life, and booked as expenditure, that is, as negatively impacting profits. The basic idea here is that, at the end of the plant's economic life, there should be enough money saved up to buy a new plant of exactly the same quality/price. Expenditure decreases profit, so it also decreases the tax-burden profits bring with them, as well as the dividend owed. 1000 MU / 25 years = 40 MU. For the 500 MU of the bank loan 5% interest is due (500 x 0.05 = 25 MU). The loan is likewise amortized over 25 years, thus; amortization equals 500 / 25 years = 20 MU. The amortization simultaneously decreases the debts on the liability side and the cash account on the asset side, which is why it's termed a “net income neutral balance sheet contraction,” [I hope I got that vaguely right!] because, with amortization, neither expense nor gain accrues. Repayment of the loan itself does not decrease profits, only payment of the interest does. Personnel costs must of course be paid in cash, since the workers need money to pay their bills and go shopping with. Wages also become earnings from the company's customers, which are likewise paid in cash.

The result of all this is a balance sheet profit of 25 MU, whereas the cash flow shows 45 MU. The calculation of profit can be established with 't-account'-presented (ledger) profit and loss accounting:

The deductions are listed as expenditure in the profit and loss accounts, even though they do not correspond with any [ongoing] disbursements. Their function is a purely numerical allocation of investment costs over the lifespan of the atomic power plant. Correspondingly, received cash earnings will not be taxed to that extent, since earnings are 'opposed' by these numerical deductions, an 'opposition' which reduces profits by that amount. This amount (40 MU) is also not due to the share holders, because profits are reduced by the deductions. The difference between earnings and expenses (in this example: revenue – personnel costs – deductions – interest) yields a profit of 25 MU. This profit is then relevant both to tax and dividend owed. But of more importance for the survival of the company is the actual cash flow. This is calculated in our example thus: revenue – personnel costs – interest – amortization = 45 MU.

Deductions are not cash entities, they are a pure numerical expense, and are therefore not payments. On the other hand loan amortization [loan repayment], while not an [accounting] expense, must nevertheless be paid out of the company's cash registers, and therefore negatively impacts cash flow. When all's said and done we get the following balance account:

The power plant was deducted by one year (1000 MU – 40 MU = 960 MU). Cash reserves have increased by the amount of the cash flow (20 MU + 45 MU = 65 MU), bank debt was amortized by one cycle (500 MU – 25 MU = 480 MU). Net assets increased by the year's profit (520 MU + 25 MU = 545 MU). And since each business event must be booked twice to be correctly calculated, we see again equal asset and liability totals in the balance sheet.

Companies must estimate their prices in such a way, in this case the price of the electricity supplied, to enable them to earn a profit. Even in this simple example, however, it's clear to see that the process of establishing price must consider something else: keeping cash flow healthy! Let's finally have a look at the balance sheet of this energy supplier at the end of the power plant's economic life, that is, in year 26. The loan is completely paid back, the power plant completely deducted, and all other data we'll assume unchanged. The following profit and loss account emerges:

Against the claim against the debtor (Claim K) is a bank liability of its assets of the same amount (Liability K). The balance total rose by the amount of the loan, of which one says, the balance extended itself by the amount of the credit.”

(Toby again.) The final paragraph is key and was extremely difficult to translate (and I don't know what “Claim K” and “Liability K” refer to). Furthermore, I have here translated an explanatory section without translating the passages it illuminates. In that light perhaps my thoughts on all this might be helpful...

In conjunction with double entry bookkeeping, in conjunction with the Central Bankers' explanation of money creation procedures (numerically booked debt is the bank 'asset' which 'backs' the created giro credit (money)), in contrast to market-based price discovery (supply and demand determining price as if by magic in the organic hubbub of 'transparent' buying and selling), and in glaring contrast to the impossible conditions of Perfect Competition, what Hoermann is here exposing is the old fashioned and humdrum, messy and guessed way in which price is set on the supply side, as well as how profits are both calculated and reported. And above we have seen the only simplest basics. I can barely imagine the tricks and chicanery Guru Accountants are capable of.

In sum, what we have here are the actual mechanics, which are deliberately counterintuitive and abstruse, of money creation and accountancy—accountancy being the discipline which tells us about profit and loss—all of which bears precious little resemblance to orthodox economics' fairy tale, The Myth of Free Markets. Hence the measuring of value via money/the price system is not only doomed by the relativity and subjectivity of value itself, but also inherently flawed and unscientific systemically. 'Out there' is a mess of the powerful maintaining their power with all manner of shenanigans, in a socioeconomic system which forces Perpetual Growth on the economic activity of one of planet earth's animals, even though the planet has finite resources.

Go figure.